[ad_1]

This article is a page of our Unhedged page. Enter Pano so that the letter can be sent to your inbox every day of the week

Welcome back. We hope our American readers enjoyed a proper mix of Thanksgiving overeating and arguing with relatives. Send me the shocking news of the holiday week, about the market or not, to me robert.armstrong@ft.com or to Ethan at ethan.wu@ft.com

Omicron

Here is the S&P 500 chart from last year. Can you choose to sell in the market during the Delta crisis? Do you remember when that happened? Do not search for Google, you scammers.

It happened in July. You can see it below the question in the chart header. Our last contact with a type of virus caused a small explosion that we all forgot about four months later.

In the past, investors who were frustrated by the closures fled trips with the power to keep green spaces like Moderna and Kroger. The oil was crushed and its composition was crushed before it returned. Advertisers began raising prices at slightly higher levels in the future, betting on a long-term low inflation policy. And within a week or so, the markets were in a state of shock.

The strategies launched in July reaffirmed themselves last week. Modern raises S&P 500 again. Oil fell by about $ 10 a barrel on Friday (although some losses were reversed when future markets reopened at the end of Sunday). The harvest cycle is broken. Investors are now expecting a median rise of 2.1 at the end of 2022, down from 2.8 early last week, according to Bloomberg. If the Delta template works, the markets are run for a nervous week followed by a strong recovery.

There’s another reason to watch Friday’s big sale. Omicron’s news has reached the world’s most important market – the US – because of its imminent rise, due to the economic recovery. growth and, perhaps more, very happy animal spirits, as Unhedged in detail last week. Everything imaginable is hot, from research to market action. It is understandable that such a market should be affected by bad news. There is no cost.

Delta’s short-term market results, as well as the natural jump of the modern market, make us sad with the summary of Barry Norris of Argonaut Capital, mentioned in FT Friday: “Knee splint is definitely a commercial. Next week the vaccine company will say their jab is working on a new type and you will be whipped again”.

As a result, Unhedged did not fall into its trap. But there are at least three reasons to think that this time could be different from July.

Financial and financial policies have changed. Prices for US points were rejected to zero when Delta hit and are in the same position today. But the rise of QE is currently in its infancy and policy growth is imminent, although Omicron (seeing the market) may delay or irritate both processes. The main difference is the rise in prices, which the Fed and central banks around the world need to keep an eye on, yet the medical crisis grows. They do not want the current state of “growthflation” to change into a permanent one.

It is unknown at this time what he will do after leaving the post. A sudden drop in electricity prices will be the first to be deflationary. Electricity prices accounted for 1.8 points of a 6.2 percent annual increase in consumer prices in October. But over time the question is whether the Omicron waves can reduce the need or provide more information, which would depend on the prevalence of local diseases and the response to the facts. As Paul Ashworth of Capital Economics puts it succinctly:

With China seeking to maintain its zero-Covid deregulation goals, the first assumption that Omicron diversity can increase inflation pressure, and exacerbate existing problems, is understandable. But it is about to be decided whether attendance will be more significant than necessary. In the worst cases when Omicron became vaccinated and highly contagious, full. [US] blockages – especially in northeastern California – cannot be eliminated, while a gradual decline will be the cause of a major crisis.

Last summer, with the first Delta crisis, many Americans received checks a month or two earlier, and some were still receiving special Federal unemployment benefits, which expired in September. The prospect of further financial support in the face of another crisis seems slim. Ed Mills, Raymond James’ commentator, explained to me yesterday:

The last financial response followed a blockage with some issues related to Covid, and because Republican authorities will not respond more than they did in March 2020 – fewer governors will issue closure orders, fewer businesses will close – forced economic response will be. down. . . Covid became involved in politics, which is why closed laws and financial responses have also become political. Things should get worse before the federal government responds.

Mills also shows systemic inconsistencies. If Democrats decide to move forward with financial support in response to Omicron’s spread, without any Republican support, they can do so through budget consolidation, and this can only happen once in the budget process. For this financial year, however, reconciliation is already being used to push the Biden “Build Back Better” bill.

A second transition with greater flexibility can have different effects on the will, attitudes, and participation of employees. because it may begin to appear as the manifestation of endangered species and a process established to repeat itself forever. As Simon Quijano-Evans of Gemcorp briefly points out, the problems are twofold:

1) A group of people in the northern hemisphere have decided that they do not want to be vaccinated, and 2) The Society in Africa has no choice in the matter of vaccination, because it was denied access to the vaccine. vaccine.

Vaccination companies are expected to launch a new vaccine in just a few months. But as long as low-vaccinated areas (Africa, Alabama) function as development labs, vaccine manufacturers seem unable to move forward with the game.

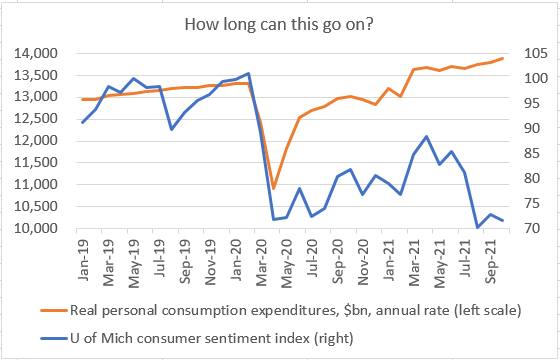

It sounded for a while as we were at the end of Covid. What happens to the economy if there is a collective awareness that we are in the middle innnings? The question is growing in the US, where consumer spending is making the economy poorer even if consumers do not like it. Covid’s other dark season could bring these two, not in a good way (Fed):

The health effects of mutation may be different. World Health Organization he thinks Risks of re-emergence from Omicron may be greater than previous versions, and story that two flights from South Africa to the Netherlands had 13 patients diagnosed with the virus is dangerous. Pali three cases in the UK already. It would be strange if this change would not be available on any continent in the coming weeks. Key questions are the development of the disease and the effectiveness of the existing vaccine (with a new small molecule). medicine) against them. It is absurd to imagine the possible consequences. But the realities of medicine are far more important than financial and policy developments.

One good reading

Very good research and my FT colleagues of the political and economic crisis facing gambling in Macau, and the exciting microcosm of Xi government policy.

[ad_2]

Source link