[ad_1]

Welcome. This is the first type of Unselected, a new FT email that is inserted into the inbox every day of the week. The theme is markets, and people and companies live and die with them. I hope to combine powerful analysis with clear and immersive speaking ideas here, when we have fun. I hope you will join us on this journey.

Enter Pano for this letter to be sent to your email. Tell your friends and email me if you think I’m a hero, stupid, all, or not: robert.armstrong@ft.com.

Last week last week? Get used to it

Last week was a dry. Last week Lousy working report (The economy is good, good in the markets because unexpected economic trends are possible) it was from Wednesday inflation report (hot, ugly, hard). It later became The Week We All Complainant Even More In Economics.

Shares, especially those who are growing up, tread like a joke on a bicycle assembly. Nasdaq fell 5% from Monday morning and Thursday afternoon. Yields rise. Then, Friday, the panic subsided, and things were about to go back to normal. From my Reuters site:

Where does this leave us this week? Breathe deeply.

The market tends to overreact, and it seems to be outraged by inflation. My old friend Matt Klein, of Barron, made a simple case to settle. More more than 60% of the increase in inflation from last month comes from things that you would expect to be temporary: “Used cars, hotels and motels, airplanes, car insurance, car and car rental, admission to events and museums , and food away from home. ”

Of course, we need to keep an eye on inflation and other signs of inflation in the coming months. No, this is not the time to be distracted.

Cattle as this point. Here is one, the head of a private business bank, e.g. quoted Fellow author Katie Martin:

Bears are always on the lookout for signs of endangered species. They come with all possible reasons. The fact is that the only important question is whether the reopening is right or not. And it is going well.

True and silent bears! (Other than that, for a decade now they have failed to follow one simple test rule you may need: once you see US goods, buy them). Yet there are at least two reasons, apart from the bears’ silence, that the market is jumping on the bandwagon. One is short, and the long.

The long-term reason for this is that the market has rapidly and strongly downgraded the coming economy and reopened. But it will soon reduce its size. This is how Omar Aguilar, CIO of several ways at Schwab, put me:

We are living in a much faster time than ever before. . . markets expect unprecedented recovery and GDP growth last year. If we assume that lower GDP is coming, the market will also be ahead of it. Hopefully we will see the pull when we reach the peak – we will reach the peak of what we know before we know it.

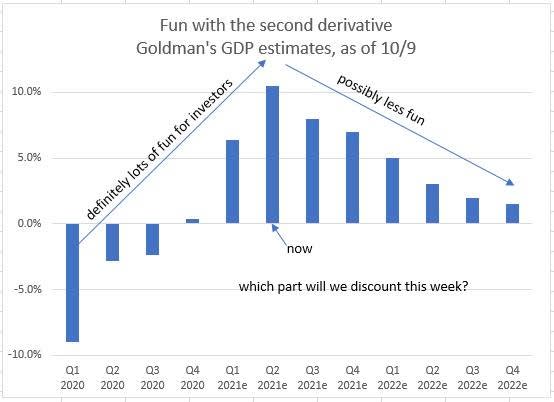

Aguilar thinks the larger size could be a little slower. Some think it is happening here. Here are Goldman’s economic group ideas for quarterly GDP growth (picture is mine, you may not know):

My boss at the hedge fund where I work often says: always look for a second source. It’s nice to have money when you’re growing bigger than it used to be. Here is what the best economist Don Rissmiller of Strategas sent me in emails about GDP decline:

2Q is a major indicator of real GDP growth in the US. . . It is also possible that 1Q 2022 will see corporate and private taxes increase, which means that there will be no slowdown, but a temporary temporary slowdown as we begin the new year. Gradually, the risk increases as the year progresses due to fewer vaccinations (excluding the possibility of another winter crisis), higher transit costs, the potential for Money to initiate negotiations on tapering, and increased taxes.

Does this make you feel like jumping? Yes, I do too.

Now the long-term point. Here is a chart that happened in FT a few weeks ago, in piece Author Karen Ward of JPMorgan:

The relationship between counting and long-term returns is imperfect, but it is as strong as any predictable relationship in the markets. If we know everything, we know that when you buy the market it is very expensive, you will not earn much money in the end. And where the calculations are right now, history tells us that the money we spend today will be back, oh, no, giving or taking a few shares, annually for the next 10 years.

Counting is useless, or worse will tell you when to sell. If you sell and miss out on a fun time at the end of the bull market, you probably won’t do well in time. There is no good reason to have a face-to-face meeting starting tomorrow.

But knowing that you have to have stocks for a short period of time, and you can’t really expect a long-term return, is the way to financial treatment. Know the weeks if last week. It will be a few years strange.

Read it carefully

I just finished Noise, a new book by Daniel Kahneman, Olivier Sibony and Cass Sunstein. It is not a very good book like Kahneman Thinking, Fast and Slow, but it does convey a very important point. Mistake-free errors (noise) in our minds are destructive and common as erroneous, irreversible in them. Thank you very much Kahneman, wise savvy investors are always thinking about favoritism and how to deal with it. They should also consider the same noise.

[ad_2]

Source link